ARTICLES

Six Compliance Signals Reflected in Customs Administrative Penalties for High-value Cases

Six Compliance Signals Reflected in Customs Administrative Penalties for High-value Cases

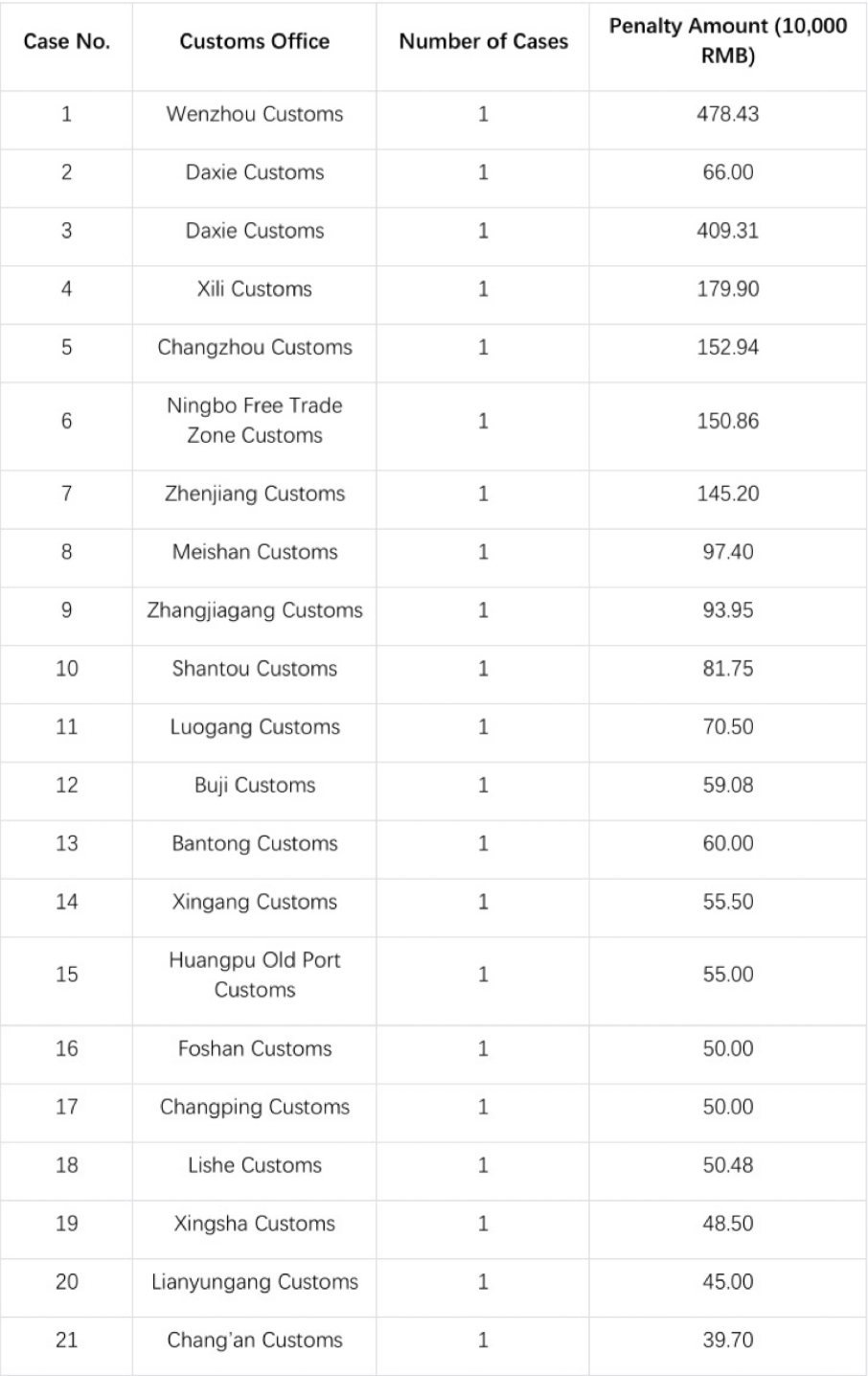

This statistical review targets administrative penalty cases publicly released via official channels of customs authorities nationwide during the period from March 16 to April 16, 2026, involving a monetary penalty of RMB 300,000 or above. All raw data are directly extracted from the administrative penalty announcements published on the official websites of the relevant customs authorities. In total, 21 cases have been adjudicated by 20 customs authorities, with the aggregate penalty amount reaching RMB 24.3950 million.

Table 1: Overview of Administrative Penalty Cases of Over RMB 300,000 Issued by Customs Authorities Nationwide (March 16 – April 16, 2026)

Compliance Signal 1: Risk Alert for Japanese-funded Enterprises

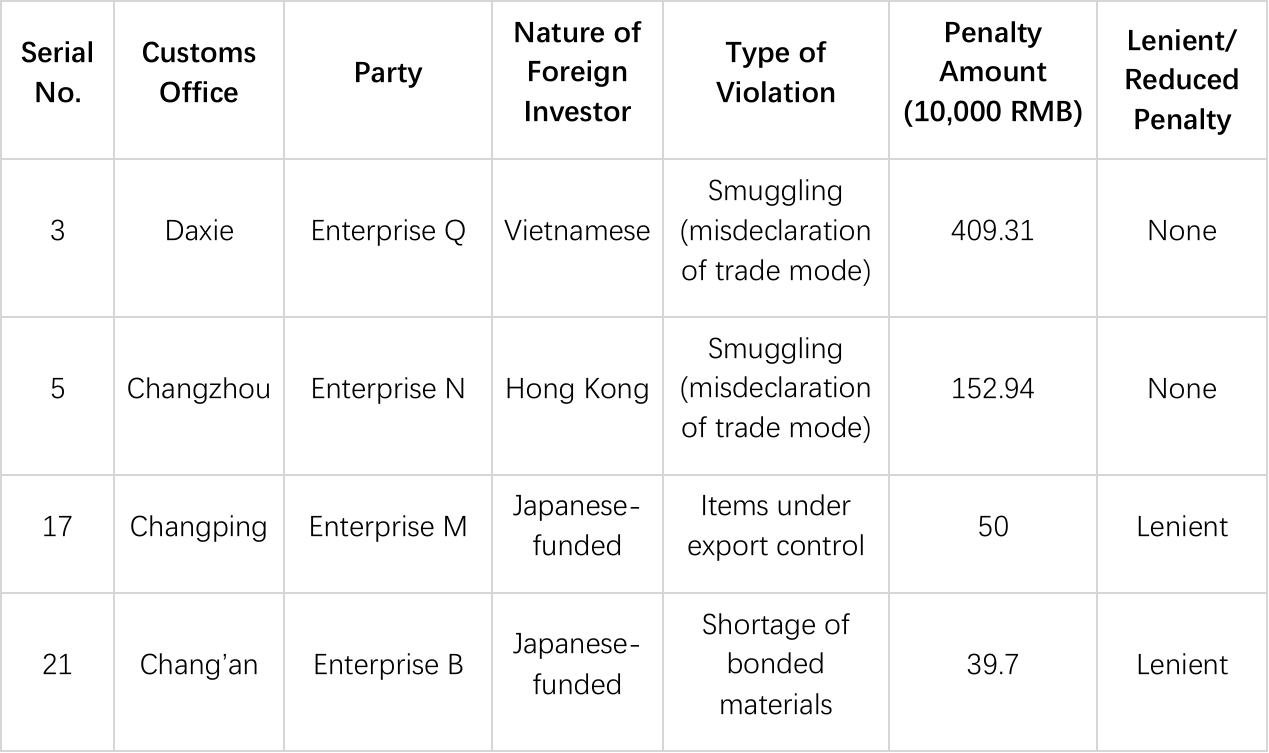

Table 2: Statistics on Violations, Penalties and Leniency of Foreign-related Enterprises by Customs

Among the cases reviewed, four involve foreign-invested enterprises, two of which are Japanese-funded: Enterprise B in Chang’an (shortage of bonded materials, lenient penalty of RMB 397,000) and Enterprise M in Changping (involvement in export-controlled items, lenient penalty of RMB 500,000). Japanese-funded enterprises in China are primarily engaged in processing trade and precision manufacturing, so cases involving bonded material management are relatively common, whereas cases involving export-controlled items were rare before 2026. However, with changes in China-Japan relations, export controls against Japan have become a focal point, and the associated enforcement risks should not be underestimated. Japanese-funded enterprises need to pay close attention to two emerging developments:

First, on January 6, 2026, the Ministry of Commerce issued Announcement No. 1 of 2026[1],which prohibits the export of all dual-use items to Japanese military end-users, for military purposes, and for any other end-use by end-users that contributes to the enhancement of Japan's military capability. This sets forth the general principle for China’s export control of dual-use items against Japan.

Second, on February 24, 2026, the Ministry of Commerce issued Announcement No. 11[2] and No. 12[3], placing 20 Japanese entities on the Export Control List, with a general prohibition on exporting dual-use items to them. Meanwhile, 20 Japanese entities were added to the Watch List, requiring stricter end-user and end-use reviews for exports to these entities.

As export control against Japan continue to tighten, Japanese-funded enterprises engaged in precision manufacturing, new materials, aerospace and other sectors shall establish a dedicated export control compliance screening mechanism, and can no longer rely on the traditional customs compliance management approach.

Compliance Signal 2: Application of Administrative Discretion Benchmarks and Standard Practices for Seeking Lenient or Mitigated Penalties

(I) Discretion Benchmarks Have Achieved Broad Coverage

Table 3: Legal Basis for Customs Administrative Penalties and Their Application in Relevant Cases

In current customs administrative penalty practice, Discretion Benchmark (I) (GAC Announcement No. 182 of 2023) applies to general customs administrative violations and solid waste supervision cases; Discretion Benchmark (II) (GAC Announcement No. 21 of 2025) applies to penalty cases involving inspection and quarantine. Among the 21 cases reviewed, except for three export control cases governed by the Export Control Law, all other cases fall within the regulatory scope of the aforesaid discretion benchmarks.

The purpose of the uniform application of discretion benchmarks is clear: to unify nationwide law enforcement standards, reduce disparities in discretion, and enable enterprises to have clear expectations on compliance and violation risks.

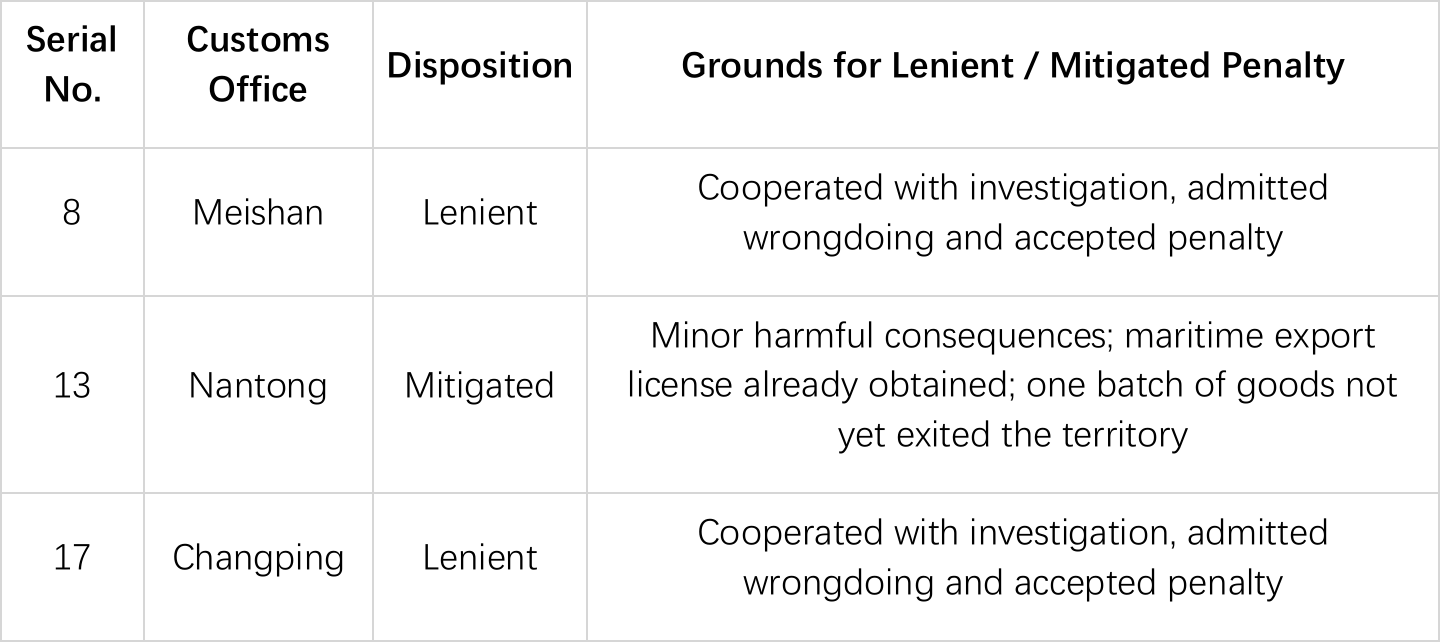

(II) “Cooperating with Investigation + Admitting Violations and Accepting Penalties”: Core Path to Leniency

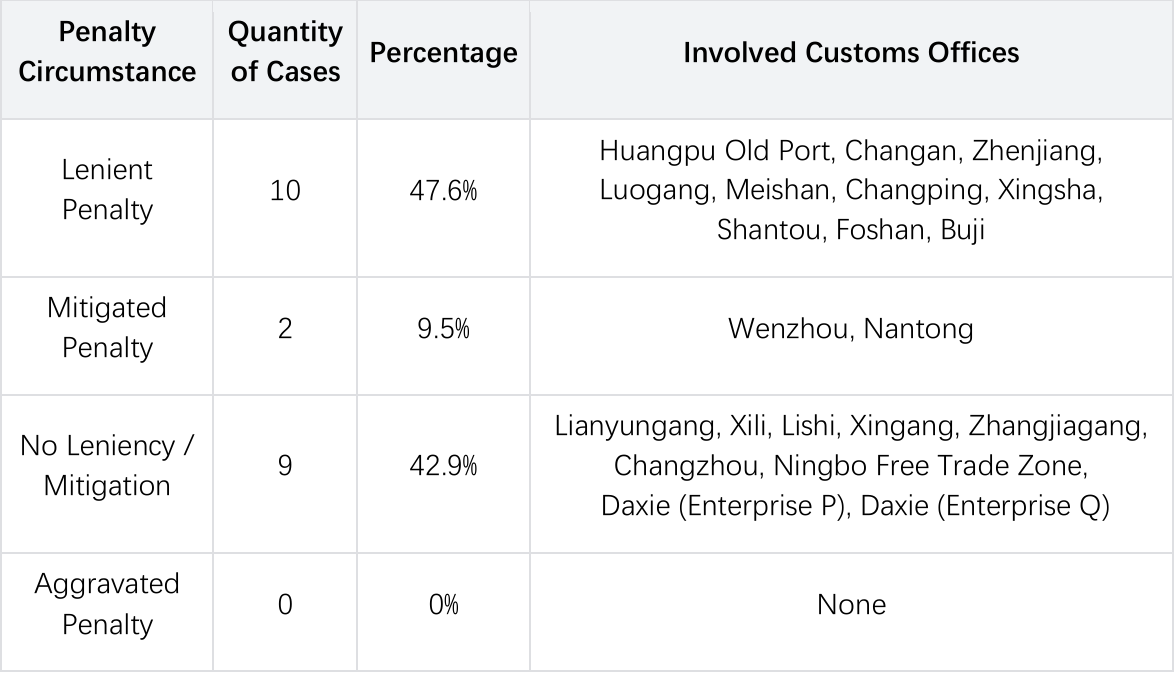

Table 4: Statistics on Cases by Penalty Circumstance

In this review, 10 cases (47.6%) received lenient penalties, 2 cases (9.5%) received mitigated penalties, 9 cases (42.9%) were neither lenient nor mitigated, and 0 cases (0%) received aggravated penalties.

All 10 lenient penalty cases are subject to Item 2 of Article 9 of the Discretion Benchmarks (I) : cooperating with customs in the investigation of illegal acts,admitting misconduct as well as accepting punishment. This clause requires two simultaneous conditions: first, actively cooperating with the investigation, assisting customs in ascertaining the facts of the case, and providing corresponding guarantees in accordance with the law;[5] second, explicitly acknowledging the illegality of the act in writing, accepting the penalty decision, and voluntarily assuming corresponding legal liabilities.[6]

The 2 mitigated penalty cases (Enterprise G in Wenzhou and Enterprise R in Nantong) applied the statutory leniency circumstance of voluntarily eliminating harmful consequences. The key distinction between mitigated and lenient penalties lies in that a mitigated penalty is imposed below the statutory scope of punishment, while a lenient penalty is imposed within the statutory scope. The core reason for the mitigation in the Wenzhou and Nantong cases is that the parties took proactive remedial measures before customs case filing, including voluntarily disclosing illegal facts, reapplying for relevant permits, and preventing the illegal outbound shipment of goods.

(III) Three Categories of Circumstances Ineligible for Leniency

Leniency is not applicable to all cases. In particular, where an offending enterprise has the following aggravating circumstances, customs authorities will generally, in practice, comprehensively consider all facts of the case in accordance with the principle of fairness and impose a penalty within the range for ordinary circumstances, even if lenient circumstances exist concurrently.[7]

1. Committing the same type of illegal act again within one year after being penalized for the same violation; pursuant to Item 2 of Article 10 of the Discretion Benchmarks, this shall be taken as a consideration factor for aggravated penalty.

2. Refusing to cooperate with the investigation, or intentionally destroying/concealing evidence of violations, demonstrating a lack of basic willingness to cooperate with law enforcement.

3. Having obvious subjective intent to smuggle while refusing to admit guilt or acknowledge established illegal facts, thus being ineligible for a lenient penalty.

Compliance Signal 3: Tightening Trend of Lenient and Mitigated Penalties Under the Export Control Law

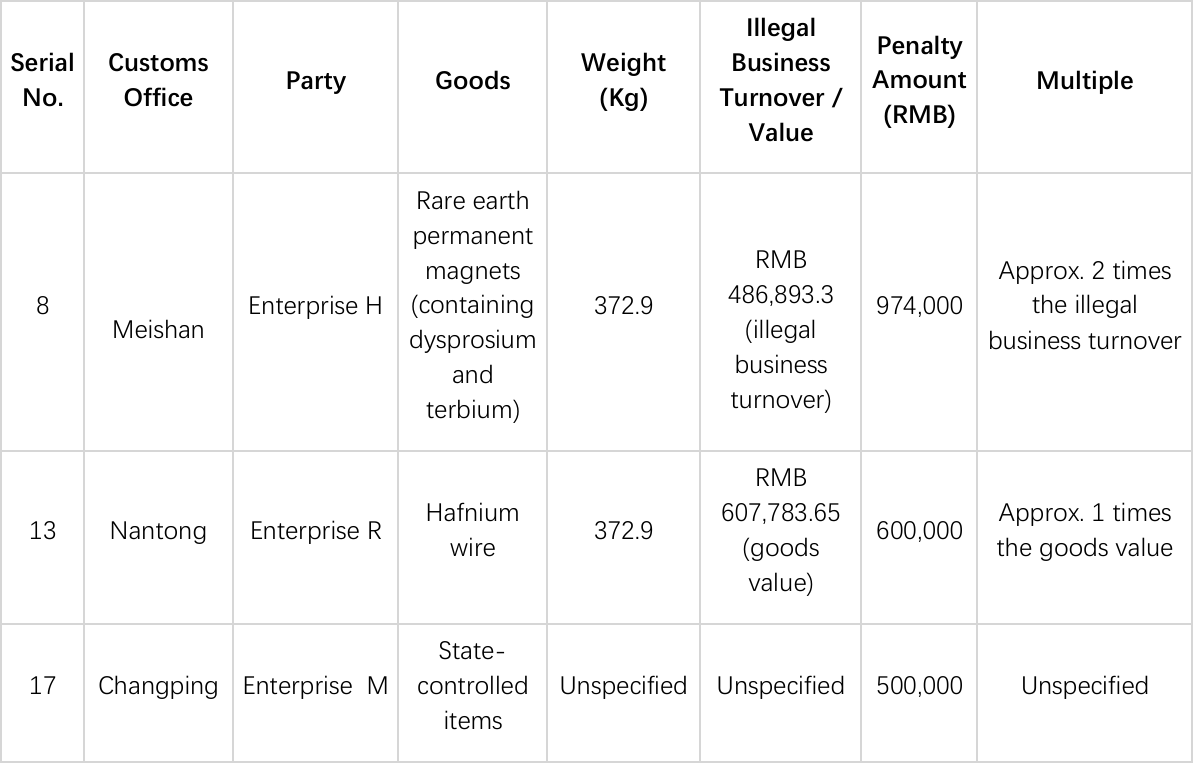

Table 5: Export Control-related Customs Administrative Penalty Cases in This Review

Table 6: Lenient and Mitigated Penalties in Customs Export Control Cases

Among the cases reviewed, three involve export control violations (Enterprise H in Meishan, Enterprise M in Changping, and Enterprise R in Nantong), all of which were granted lenient or mitigated penalties. This trend needs to be understood from a broader perspective.

In the Meishan case, the party illegally exported rare earth permanent magnets containing dysprosium and terbium, with an illegal business turnover of approximately RMB 486,900 and a penalty of RMB 974,000. The Changping case incurred a penalty of RMB 500,000. The Nantong case involved hafnium wire valued at about RMB 607,800, with a penalty of RMB 600,000. Among the three cases, the Meishan and Changping cases were granted lenient penalties, while the Nantong case was given a mitigated penalty.

Export control violation cases have generally received lenient treatment in practice. However, it is noteworthy that prior to 2024, customs authorities frequently applied Article 32 of the Administrative Penalty Law to cap penalties at a relatively low level, namely within the scope stipulated by the Regulations on the Implementation of Customs Administrative Penalties[8] (capping within 30% of the goods value). Such lenient penalty has decreased markedly since 2025. It is expected that customs law enforcement will likely be further intensified, and compliance requirements for enterprises will be raised to a higher standard.

Compliance Signal 4: Contested Boundary Between Inaccurate Declaration and Smuggling

(I) Comparison between Case 7 (Zhenjiang Customs) and Case 10 (Shantou Customs)

Both Case 7 (Zhenjiang Customs) and Case 10 (Shantou Customs) constitute major inaccurate declaration incidents, but were characterized and disposed of as administrative violations rather than smuggling. The core difference lies in the difficulty of proving “subjective intent” and the reasonableness of commodity classification.

Case 7 (Zhenjiang Customs): From July 2023 to July 2025, Enterprise C exported 32 batches of photovoltaic ribbons. It falsely declared the applicable HS code as 8311300000 instead of the correct codes 74081900 / 74091190, resulting in an excess export tax rebate of RMB 1.8853 million. In the author’s view, as an emerging product, photovoltaic ribbons fall into a grey area of classification between heading 7408 (copper alloy wire/strip) and heading 8311 (soldering products). Specifically, heading 7408 covers copper wire and heading 7409 covers copper sheet and strip, both categorized as copper and basic copper products, classified mainly by material and cross-sectional shape. Heading 8311 applies to base metal strips and wires flux-coated or flux-cored for brazing and gas welding purposes. Photovoltaic ribbons are made of high-purity copper as the base material, mostly in a rectangular flat ribbon form, with a tin-lead alloy coating on the surface. It possesses the attributes of a metallic base material, an electrical connection function, and a solderable coating characteristic, naturally touching upon the defined scope of multiple tariff headings above. Since the Chapters and General Notes to the Tariff Schedule do not draw an absolutely clear dividing line on the morphological boundary between wire and strip, nor between flux coating and ordinary functional coating, and given the composite properties of photovoltaic ribbons including conductivity, structural connection and solderability, different stakeholders can all find supporting tariff basis for their classification claims from the perspectives of material, shape, coating, core function and designated application. Accordingly, there exists statutory and reasonable room for classification dispute for photovoltaic ribbons among HS codes 7408, 7409 and 8311. The export tax rebate rate of HS code 8311300000 was once 13%, adjusted to 0% on December 1, 2024; the rebate rate for 7408/7409 is also 0%. The party could reasonably claim a classification discrepancy rather than intentional misdeclaration. Customs finally ruled it as inaccurate commodity code declaration instead of smuggling, primarily due to insufficient evidence to prove subjective intent.

Case 10 (Shantou Customs): From February 2023 to May 2024, Enterprise S imported 44,546 cameras via the bonded cross-border e-commerce model, declaring under HS code 85258929 while the correct code should be 90064000. In terms of tariff heading attributes, HS 85258929 falls under Chapter 85 Electrical Equipment, covering non-special, non-DSLR, non-interchangeable lens digital cameras. Such cameras adopt the photoelectric conversion principle, forming images through lenses, capturing signals via image sensors and converting them into digital electrical signals stored as digital files without physical film involvement. HS 90064000 belongs to Chapter 90 Optical, Photographic and Cinematographic Instruments, covering instant cameras that generate physical photos directly through photochemical instant imaging based on film exposure and chemical reaction of built-in reagents. The two differ markedly in product form, function, and use. In the author’s view, there is essentially no room for a classification dispute between headings 8525 and 9006. Yet this case was ultimately characterized only as a violation of “misdeclaration affecting tax collection and regulatory order.” Customs did not find smuggling, presumably because the party attributed the declaration error to system interface errors or third-party negligence, making it impossible to prove subjective intent. Regrettably, the administrative penalty decision contains no elaboration on relevant facts.

A comparison of the two cases indicates that whether a product itself has room for classification dispute directly determines the difficulty of proving subjective intent. Even though Case 10 (Shantou Customs) has minimal classification ambiguity, customs still adopted an administrative violation characterization, indicating that in actual law enforcement practice, the evidentiary requirements for establishing “subjective intent” are relatively high.

(II) Case 19 (Xingsha Customs): Particular Difficulties in Criminalization of Commodity Inspection Evasion

In Case 19 (Xingsha Customs), Enterprise J exported 51 batches of potassium humate from October 2021 to June 2023, with a total goods value of RMB 8.0479 million. It falsely declared the applicable HS code as 3824999999 (without inspection and quarantine control requirements) instead of 3105909000 (Inspection and Quarantine Category N, commodities subject to mandatory export inspection). Customs ruled the act as “false declaration of commodity name and HS code, and exporting commodities subject to statutory inspection without applying for inspection”, using the term “false declaration” yet imposing only an administrative penalty.

The misuse of a tariff codes presents particular difficulties in proving an intent to evade commodity inspection. Generally, not all goods under one HS code fall within the scope of statutory inspection. One tariff code may cover a variety of specific commodities, some of which may be subject to inspection and others not. Therefore, an incorrect tariff code is often not directly correlated with the inspection attributes of the goods, making it difficult to charge that the tariff code error was deliberately made to evade commodity inspection. Nationwide, there are no more than five cases per year in which charges of evading commodity inspection are brought. Accordingly, even where the value of the goods reaches RMB 8.0479 million — exceeding the criminal filing threshold of RMB 3 million for the crime of evading commodity inspection — customs may still handle the case as an administrative violation due to insufficient evidence of “subjective intent.”

(III) Case 12 (Buji Customs): The Boundary Between Administrative and Criminal Liability for Unauthorized Transfer of Bonded Goods

In Case 12 (Buji Customs), Enterprise U unauthorizedly transferred 94 bonded injection molding machines to domestic end-users from February to April 1998. The involved goods were valued at RMB 8.44 million, with dutiable taxes of RMB 1.763 million. Customs characterized the act as “a violation of customs supervision provisions”, rather than smuggling.

The case reflects a long-standing controversy over whether unauthorized transfer of customs supervised goods is subject to administrative penalty or criminal liability. Article 82 of the Customs Law of the PRC defines “selling goods under customs supervision within the territory without customs approval” as a smuggling act, while Article 18 of the Regulations on the Implementation of Customs Administrative Penalties classifies “unauthorized transfer of customs supervised goods without approval” as a regulatory violation.

In practice, cases that are commonly dealt with only as administrative matters often fall within the situation of “Three Consistencies and No Discrepancy”: replacement with products of the same variety, same specification and same model, involving no substantial tax discrepancy. The case may involve historical factors such as product replacement in practical handling.

Compliance Signal 5: Administrative Penalties Following Criminal-to-Administrative Conversion Can Be Equally Severe

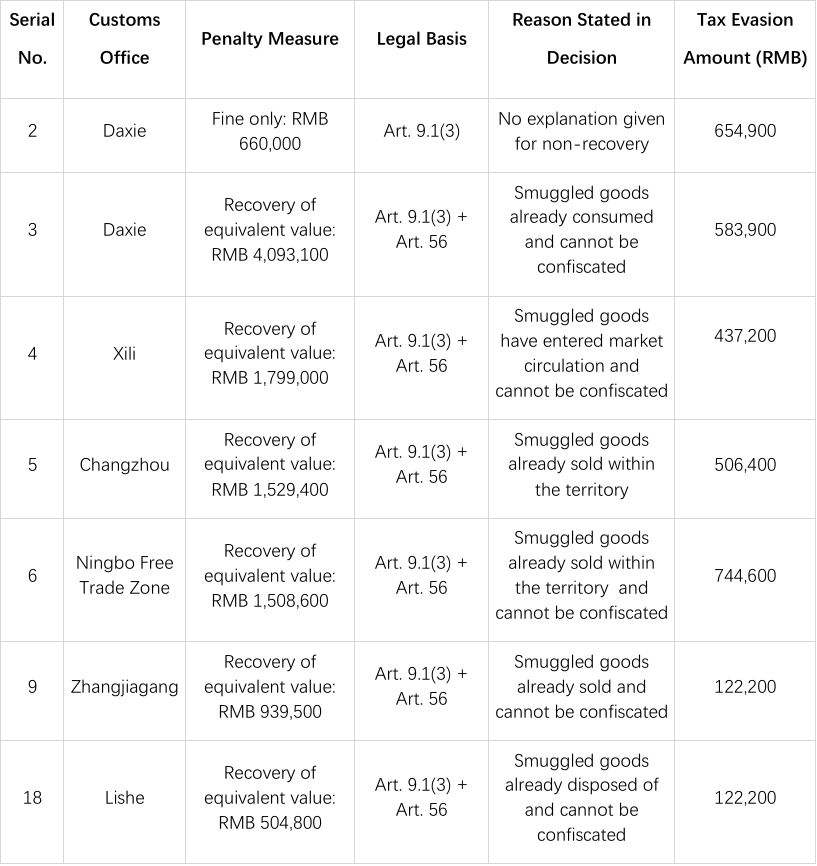

Of the 8 smuggling-related cases reviewed, 7 involve smuggling of ordinary goods, and 1 (Case 8, Meishan Customs) involves smuggling of prohibited and restricted goods. Among them, 5 cases exceed the RMB 200,000 criminal filing threshold for unit smuggling ordinary goods.

The penalty decision in Case 4 (Xili Customs) expressly states “non-prosecution by the procuratorate,” reflecting the typical mechanism of “reverse criminal-administrative conversion mechanism”: the case is first transferred to the procuratorial authority, and after the procuratorate decides not to prosecute, the case is referred back to Customs for the imposition of an administrative penalty. The other 4 cases that met the prosecution threshold but made no mention of criminal proceedings are likely to follow the same pattern.

A non-prosecution decision does not mean a reduction in financial liability. Statistics from the reviewed cases show as follows:

Table 7: Comparison of Penalty Measures and Tax Evasion Amounts in Customs Smuggling Cases

Except for Case 2 (Daxie Customs), which was only imposed a fine due to the particularity of smuggling arising from the verification and cancellation of processing trade manuals, the penalty amounts of all other cases far exceeded the actual tax evasion amounts. The recovery of the equivalent value is calculated on the basis of the dutiable price of goods, rather than being limited to the amount of tax evaded.

Huang Zhiyong and Lin Shuyan from the Collaborative Innovation Center for Judicial Civilization pointed out in their paper Research on “Administrative-Criminal Linkage” in Smuggling Cases: For smuggled goods that have been circulated and cannot be confiscated, criminal proceedings generally no longer recover their equivalent value, and only impose fines on the perpetrators. By contrast, in administrative penalties, where smuggled goods cannot or are inconvenient to be confiscated, the recovery of equivalent value is mandatory. Even if only the cargo value corresponding to the under-declared portion is recovered, the economic losses borne by the parties may still be far higher than criminal fines, giving rise to an inverted relationship between administrative and criminal penalties.

This means even if an enterprise is ultimately exempted from criminal liability, it may still face multiple adverse consequences after being referred back to Customs for administrative penalty, including full recovery of equivalent value, fines, and credit downgrade. “No criminal liability” does not mean “no penalty”, nor does it mean a lighter penalty.

Compliance Signal 6: Cross-Border E-Commerce Has Become a High-Risk Zone for Severe Penalties

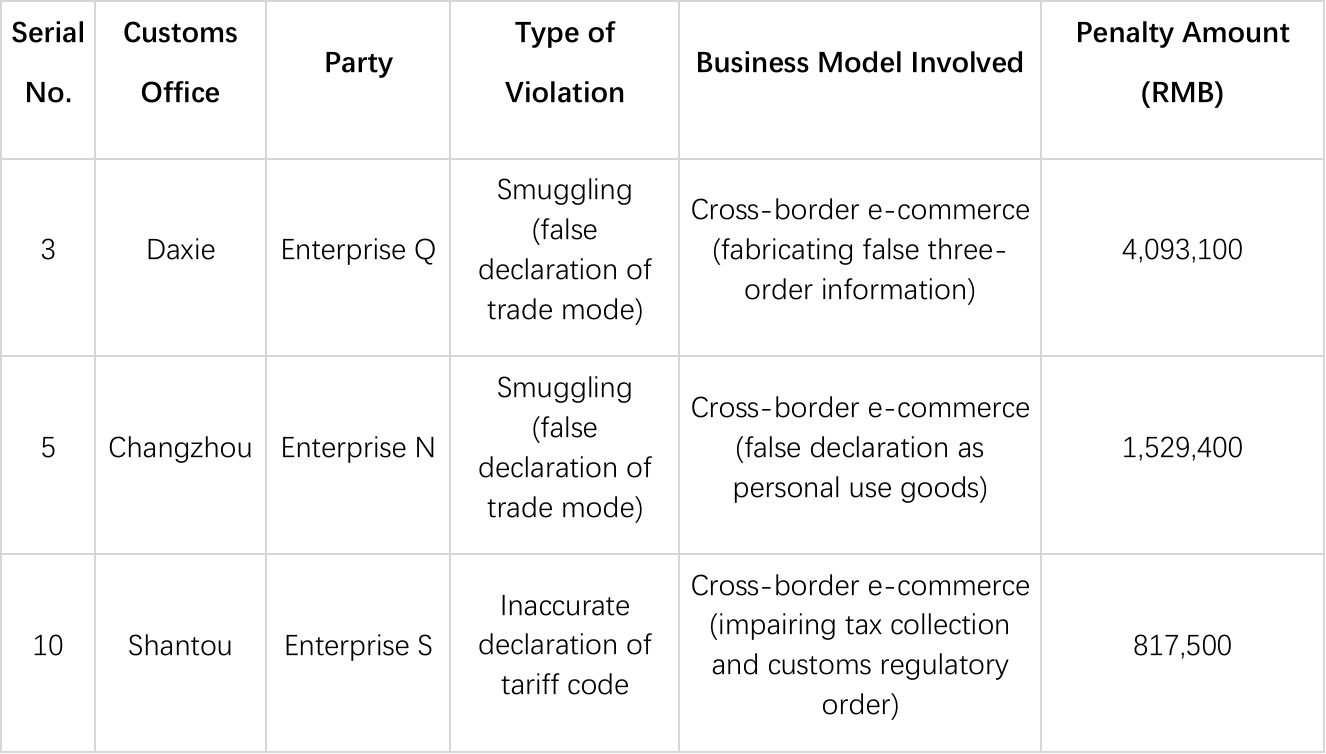

Table 8: Cross-Border E-Commerce Cases in This Review

Among the 21 cases reviewed, 3 cases involve cross-border e-commerce: Shantou Enterprise S (incorrect declaration, RMB 817,500), Changzhou Enterprise N (smuggling, RMB 1,529,400), and Daxie Enterprise Q (smuggling, RMB 4,093,100). While these three cases account for 14.3% of the total number of cases, the aggregate penalty amount reaches RMB 6,439,900 — representing 26.4% of the total penalty amount across all cases. Though few in number, their share of the total penalty amount is disproportionately high.

The three cases involve different illegal circumstances but are all associated with the regulatory channel for cross-border e-commerce:

Shantou Enterprise S imported 44,506 cameras under a bonded e-commerce model, declaring HS code 85258929 (television reception apparatus) when the correct code should have been 90064000 (cameras), constituting an incorrect declaration that affected tax collection and the regulatory order. The party took advantage of the regulatory convenience of bonded cross-border e-commerce warehousing, but made an incorrect HS code declaration.

Changzhou Enterprise N adopted methods of using others’ purchase quotas and placing fake orders to stockpile goods, falsely declaring fish oil capsules — which should have been imported under general trade — as cross-border e-commerce personal articles to smuggle them into the country, evading customs duties of RMB 506,400, and was ordered to undergo equivalent value recovery of RMB 1,529,400.

Daxie Enterprise Q smuggled 78,224 piecesof cosmetics, skin care products, and other goods spanning 418 product names by falsely declaring the trade mode, with a dutiable value of RMB 4,093,100, and was ordered to make equivalent value recovery of RMB 4,093,100.

In the first case, the conduct was identified as false declaration; the latter two cases both involved typical fabrication of the “three orders” — creating false orders, false payment orders, and false logistics waybills — to disguise general trade goods as cross-border e-commerce personal articles, thereby evading customs supervision and tax payment obligations. The cross-border e-commerce sector has become a high-risk zone for compliance. The data reveal two clear trends in cross-border e-commerce cases: first, the amounts involved in violations are generally high, with the average penalty for these three cases being RMB 2,146,600, far exceeding the overall reviewed cases average of RMB 1,161,700; second, the methods of violation are highly concentrated in false declaration of trade mode and “three orders” fabrication, reflecting an imbalance between the tax incentives of cross-border e-commerce and the compliance obligations of certain enterprises. For enterprises using cross-border e-commerce as a business channel, establishing mechanisms to verify genuine transaction backgrounds and review the consistency of the “three orders” is no longer optional but a necessary compliance investment.

Conclusion

However, against the backdrop of trade controls increasingly becoming a tool for national governance and international competition, we intends to share the conclusions of this monthly analysis report with the enterprises. The six compliance signals and enforcement trends highlighted above merit attention. Due to the limited disclosure of information in some case documents, not all details could be exhaustively covered. Enterprises should, in light of their own business characteristics, establish targeted compliance screening and risk early-warning mechanisms when referring to this report.

[注]

[1] MOFCOM Announcement No. 1 of 2026, Announcement on Strengthening Export Control of Dual-Use Items to Japan,https://www.mofcom.gov.cn/zwgk/zcfb/art/2026/art_8990fedae8fa462eb02cc9bae5034e91.html.

[2] MOFCOM Announcement No. 11 of 2026, Announcement on Listing 20 Japanese Entities in the Export Control List,https://www.mofcom.gov.cn/zcfb/blgg/art/2026/art_723dc334072d458b8bd508496eaa2670.html.

[3] MOFCOM Announcement No. 12 of 2026, Announcement on Listing 20 Japanese Entities in the Watch List,https://www.mofcom.gov.cn/zcfb/blgg/art/2026/art_cfacd88ebce04b4c8c55e2048b2ef088.html.

[4] Administrative penalty cases involving customs protection of intellectual property rights shall be governed by the Customs Administrative Penalty Discretionary Benchmark (III) of PRC . As none of the cases covered in this review fall into this category, no further discussion is provided.

[5] Article 19 of the Customs Administrative Penalty Discretion Benchmark (I): Cooperating with customs in investigating illegal acts means the party concerned assists customs in investigating relevant violations to clarify case facts and facilitate disposition, and provides corresponding security to customs in accordance with the law.

[6] Article 19 of the Customs Administrative Penalty Discretion Benchmark (I): Admitting wrongdoing and accepting penalty means the party concerned truthfully confesses its illegal acts of its own will, raises no objection to the illegal facts found by customs, and expresses willingness to accept the customs penalty in writing.

[7] Article 3 of the Customs Administrative Penalty Discretion Benchmark (I) : The Customs shall base the imposition of administrative penalty on facts and take law as the criterion, and the handling decision made shall be commensurate with the facts, nature, circumstances of an illegal act and the degree of social harm.

Article 5 of the Customs Administrative Penalty Discretion Benchmark (I) : Where the same illegal act of a party has several different punishment circumstances at the same time, a decision on handling shall be made in accordance with the principles provided for in Article 3 hereof and in light of the circumstances of the whole case.

[8] Article 14,Item 1 of the Regulations on the Implementation of Customs Administrative Penalties: Where any person violates state regulations on import and export administration and imports or exports goods subject to state restrictions on import and export, and fails to present the required license documents to customs upon declaration, the goods shall be denied release and a fine of not exceeding 30% of the goods value shall be imposed.