ARTICLES

Six Compliance Signals Reflected in Customs Administrative Penalties for High-value Cases (2026.4-5)

Six Compliance Signals Reflected in Customs Administrative Penalties for High-value Cases (2026.4-5)

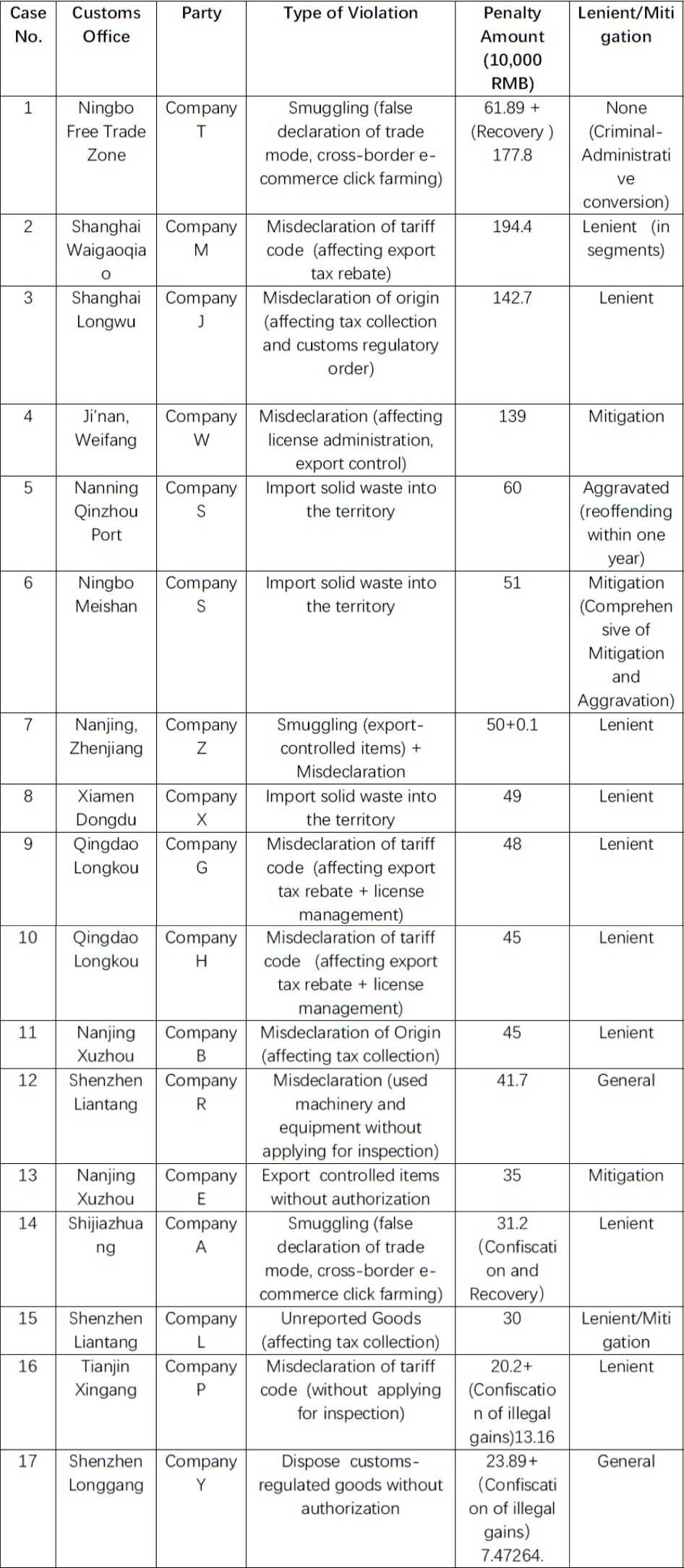

This statistical review focuses on administrative penalty cases publicly released through the official channels of customs authorities nationwide from April 17 to May 17, 2026, with penalty amounts of RMB 300,000 or above. All raw data were directly obtained from the administrative penalty disclosure information published on the official websites of the relevant customs authorities. This issue covers a total of 17 cases, each issued by a different customs authority, with total penalties amounting to approximately RMB 10.69 million, as illustrated in Table 1.

Table 1: Overview of Administrative Penalty Cases of over RMB 300,000 Issued by Customs Authorities Nationwide (April to May, 2026)

These cases are categorized by type of violation: taxable cases 8 items (52.9%), export control cases 3 items (17.6%), solid waste cases 3 items (17.6%), inspection and quarantine cases 2 items (11.8%), unauthorized disposal of regulated goods 1 item (5.9%).

Among these, the taxable cases are specifically categorized as follows: general imports (3 cases); export rebates (3 cases); and cross-border e-commerce imports (2 cases).

Compliance Signal 1: Misdeclaration of Origin Has Become a Focal Point in the Context of the Trade War

(I) Concentrated Emergence of Integrated Circuit Origin Cases

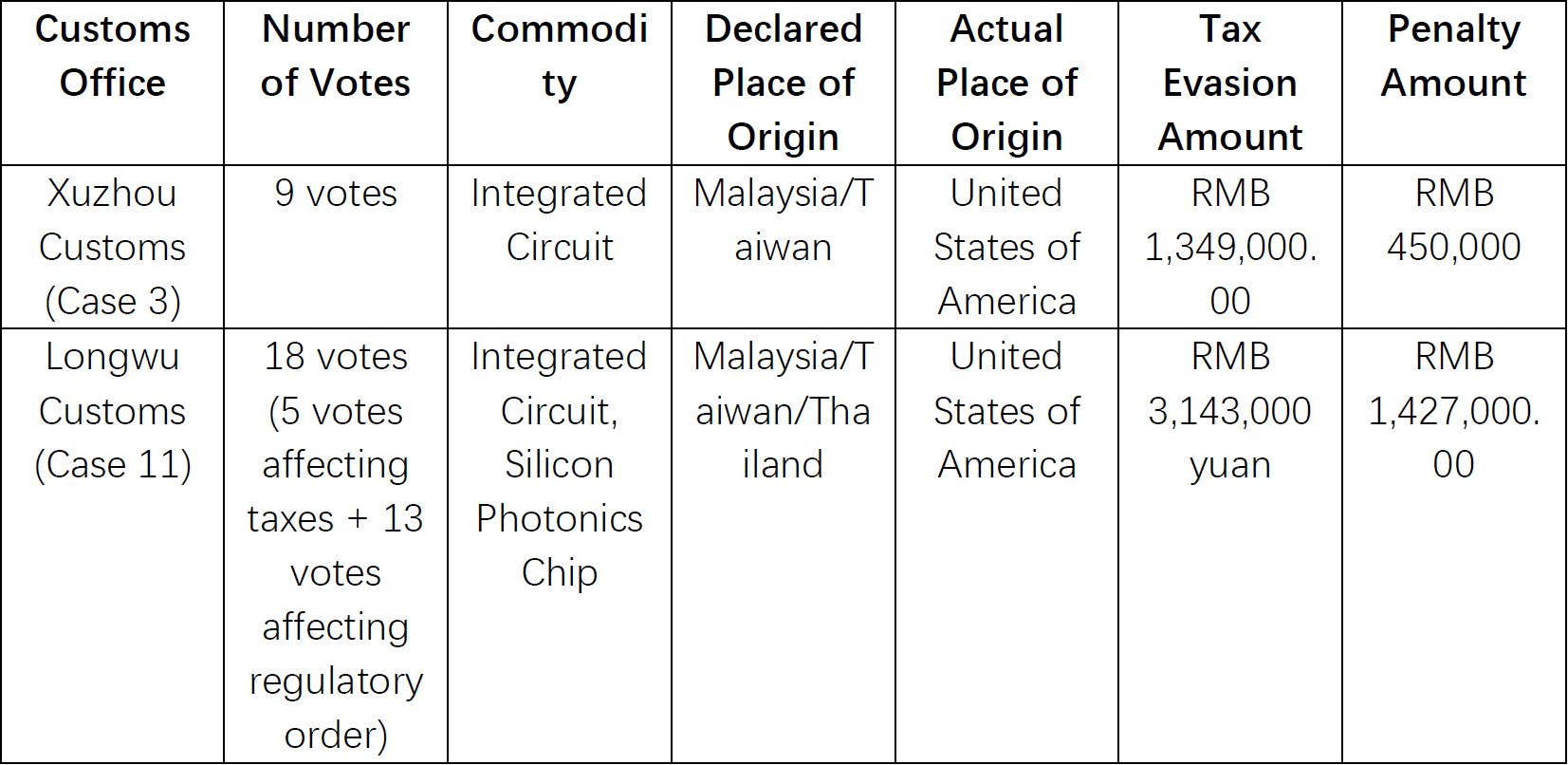

Among the 17 cases, 2 involve misdeclarations of origin, all of which pertain to the importation of integrated circuits, with the origin declared as the United States being falsely stated as Malaysia, Taiwan, China, or Thailand. The customs authorities determined that the amount of tax evasion in these cases exceeded RMB one million . This represents a new trend in 2026 among customs cases involving high-value penalties.

Table 2: Comparison of Cases Involving Misdeclaration of Origin

(II) Why Have Origin-Related Issues Become a Focal Point Currently?

1. Sustained U.S.-China trade tensions and tariff barriers remain in place. Since 2025, the United States has continued to tighten export controls on semiconductors to China, while China has simultaneously escalated its retaliatory tariffs. Although integrated circuits are strategic material, not all integrated circuits are included in the exemption list of tariffs imposed by the United States. This has greatly incentivized enterprises to evade tariffs via origin misdeclaration, making origin authenticity a core priority of customs inspections.

2. The complexity of Rules of Origin: The determination of the origin of integrated circuits involves different interpretations regarding the "substantial transformation".

Based on the Regulations of the People's Republic of China on Place of Origin of Imports and Exports and the Provisions on the Criteria for Substantial Transformation in Non-Preferential Rules of Origin, "substantial transformation" under China's non-preferential rules of origin is determined by a change in the first four digits of the HS code1. However, in practice, the wafer fabrication location is considered to better reflect the certain products. Consequently, if there are multiple wafer fabrication locations, or if an enterprise declares only the packaging location as the origin, there may be a mistake.

3. Enhancement of Customs’ Origin Tracing Capabilities: Through supply chain review, chip marking (such as wafer fabrication plant codes and packaging and testing location information), BOM list comparison, and other means, customs can more accurately identify the genuine origin.

(III) The Boundary Between Misdeclaration of Origin and Smuggling

In the case of Company B (Case 11) and Company J (Case 3), smuggling was not established. The reason lies in the fact that if errors or discrepancies arising from misunderstanding complex rules of origin occur, such conduct is generally not considered as intentional falsely declaration of origin. In practice, the General Administration of Customs is also adopting certain standards that are more aligned with industry practices to determine substantial transformation.

Compliance Signal 2: Escalation from Isolated Incidents to Massive in Export Tax Refund Cases

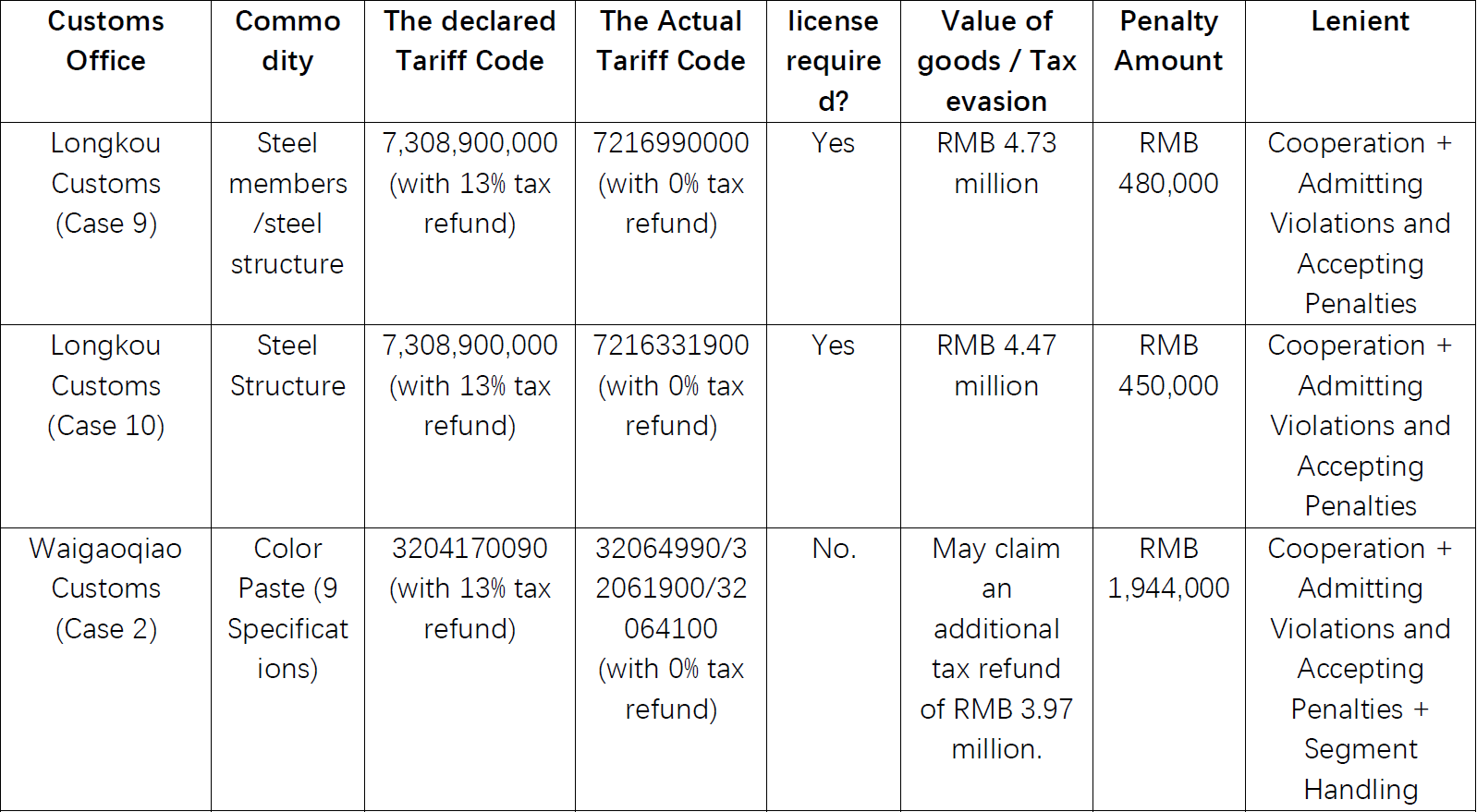

(I) Core Commonality: False Declaration of Tariff Code

Table 3: Comparison of Export Tax Refund Cases

(II) Whether the penalties in the state-owned enterprise[1] are clearly lighter than in the non state-owned enterprises, like M Company case?

In the case of Company M (Case 2), the Customs applied Article 15(1)(5) of the Implementation of Customs Administrative Penalty (pertaining to the impact on export tax refund administration)[2], and attempted to apply a refined approach. With regard to 275 entries over a period of three years (from April 2022 to April 2025), the Customs adopted a segmented handling approach: 80 entries were not subject to penalty because they exceeded the two-year statute of limitations for administrative penalties, as determined under Article 36(1) of Administrative Sanctioning Law[3]; 15 entries were not penalized because there was sufficient evidence demonstrating that the party had no subjective fault, as determined under Article 33(2) of Administrative Penalty Law and Article 7(1)(3) of the Discretion Benchmark of Customs Administrative Penalties (I) (Announcement No. 182 [2023] of the General Administration of Customs)[4]. Consequently, only 180 entries were subject to penalty, with a total fine of RMB 1,944,000.

In the two state-owned enterprise cases (Cases 9 and 10), the Customs applied Article 15(1)(3) (pertaining to the impact on license administration) and Article 15(1)(5) (pertaining to the impact on export tax refund administration) of the Implementation of Customs Administrative Penalty[5]. However, penalties were only imposed for violations affecting export tax refund administration. The reason is that the penalty decisions in both cases explicitly cited Article 29 of the Administrative Penalty Law, which states: "For the same illegal act by a party, administrative fines shall not be imposed more than once. If the same illegal act violates multiple legal provisions that prescribe fines, the provision imposing the higher fine shall be applied." This is the so-called "One Act, Heavier Penalty" principle.

From these several export tax refund cases, it can be seen that Customs is striving for refined cases handling and more accurate application of relevant regulations. It is not a special treatment for state-owned enterprises. What is worth noting is that, according to the regulation of "high fine amount", in practice, the fines stipulated in the terms are directly compared, rather than applying the terms separately and then comparing which amount is higher.

Compliance Signal 3: Customs Supervision Focuses on the Process; Penalty May Still Apply Even Without Tax Shortfalls

(I) Case 15: The Case of Company L’s Failure to Declare Goods by International Transshipment

On January 30, 2026, Company L (Case No. 15) entrusted the vehicle Yue xxxxx Gang to declare imports of "photographic paper" and other goods via the Liantang Port under the customs supervision model for international transshipment goods within customs supervision zone. During Customs inspection, unreported goods, such as earphones were discovered, and the natural wooden pallets of the unreported goods were inconsistent with the packaging type declared. This misdeclaration resulted in tax underpayment of RMB 487,960.48.

International transit goods theoretically do not pose a risk of import duties. However, in the case of Company L (Case 15), due to the failure to declare the actual goods (such as earphones), the customs still considered it as misdeclaration and affected the collection of taxes. This indicates that even if a certain trade method is "naturally tax-free", as long as it does not actively declare and accept supervision, it may still face administrative penalties for "underpayment of taxes", and the penalty amount is calculated based on the the amount of underpaid taxes.

(II) Case 17: The Case of Company Y’s Unauthorized Disposal of Bonded Materials

From October 2023 to April 2025, Company Y (Case 17), without customs authorization, delivered bonded materials— quartz watch movements (with hands and batteries)— to others, who then processed them into finished watches, which were subsequently re-exported by the party through a processing trade manual. This act removed bonded goods from customs supervision. The case involved a total of 373,632 pieces of bonded materials: quartz watch movements (with hands and batteries), with the value of the illegal goods amounting to RMB 1,991,096.53, and the party received illegal proceeds of RMB 74,726.40. The Longgang Customs imposed a fine of RMB 238,900 on Company Y in accordance with the Article 18(1)(1) of the Implementation of Customs Administrative Penalty[6], and confiscated the illegal proceeds of RMB 74,726.40.

Although the finished watches were later re-exported through a processing trade manual, this act caused the supervised goods to fall outside of customs control. As a result, the company was fined and its illegal gains were confiscated. This illustrates that whether bonded materials are ultimately re-exported does not affect the customs' phased suspension of supervision over the intermediate handling stages; unauthorized external dispatch, delivery or disposal of bonded materials still may result in fines and confiscation of illegal gains as penalties. Even if the goods eventually exit the country, it will not be considered as having eliminated the harmful consequences and thus receive a lighter punishment.

Compliance Signal 4: High Persistence of Click Farming and Smuggling in Cross-border E-commerce

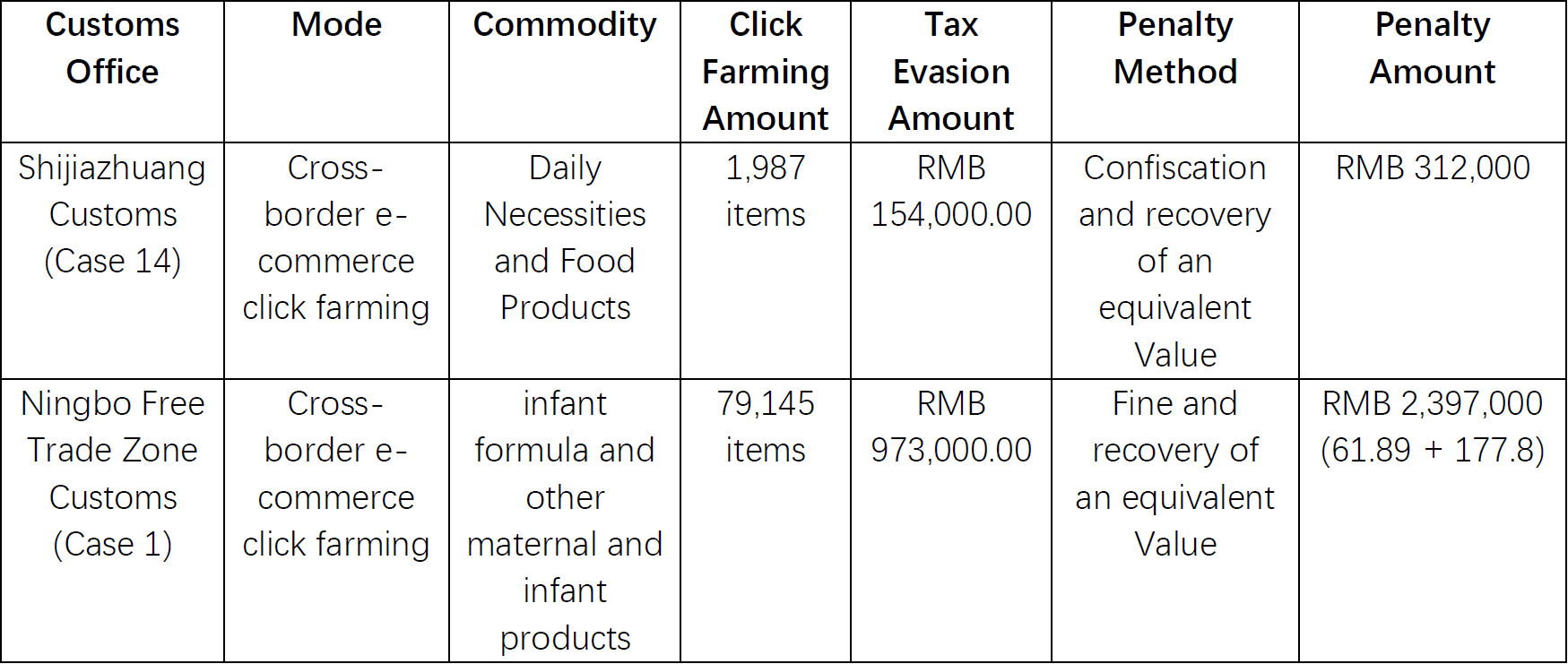

(I) Comparison of Two Cross-Border E-Commerce Click Farming Cases

Table 4: Comparison of Cross-Border E-Commerce Cases

(II) Why Are Cross-Border E-Commerce Cases More Likely to Result in Smuggling Charges?

On November 28, 2018, the Ministry of Commerce and five other ministries jointly issued the Notice of Improving the Supervision over Cross-border E-commerce Retail Imports, which clearly stipulates that where individuals illegally engage in cross-border e-commerce retail import business by using the identity information of other citizens, it shall be handled as smuggling violations and refer the case to the relevant authorities for handling in accordance with the laws and regulations concerning the illegal use of personal information. In cross-border e-commerce cases if one uses others' identity information to inflate order volumes, if they falsely declare general trade as cross-border e-commerce retail imports, it constitutes false declaration of the trade method. This kind of tax evasion behavior that accumulates small amounts through using an ID card is often not noticed at the beginning due to its low threshold. When it is discovered and filed for investigation, the amounts involved are usually large and it is abundantly clear that it was done "intentionally" with conclusive evidence. As shown in Table 4, cases 1 and 14 both constitute smuggling.

Case T (Case 1) is clearly underpinned by a "criminal judgment, decision of non-prosecution" background and falls within the category of "criminal to administrative reverse coordination" cases. In this case, the amount of penalty and recovery (2.3946 million) far exceeded the amount of tax evasion (972,700). It can be seen that in fact, a decision of non-prosecution does not equate to a reduction in economic liability; administrative penalties may be heavier than criminal fines.

Compliance Signal 5: Violation of Export Control Laws Does Not Necessarily Involve Misdeclarations

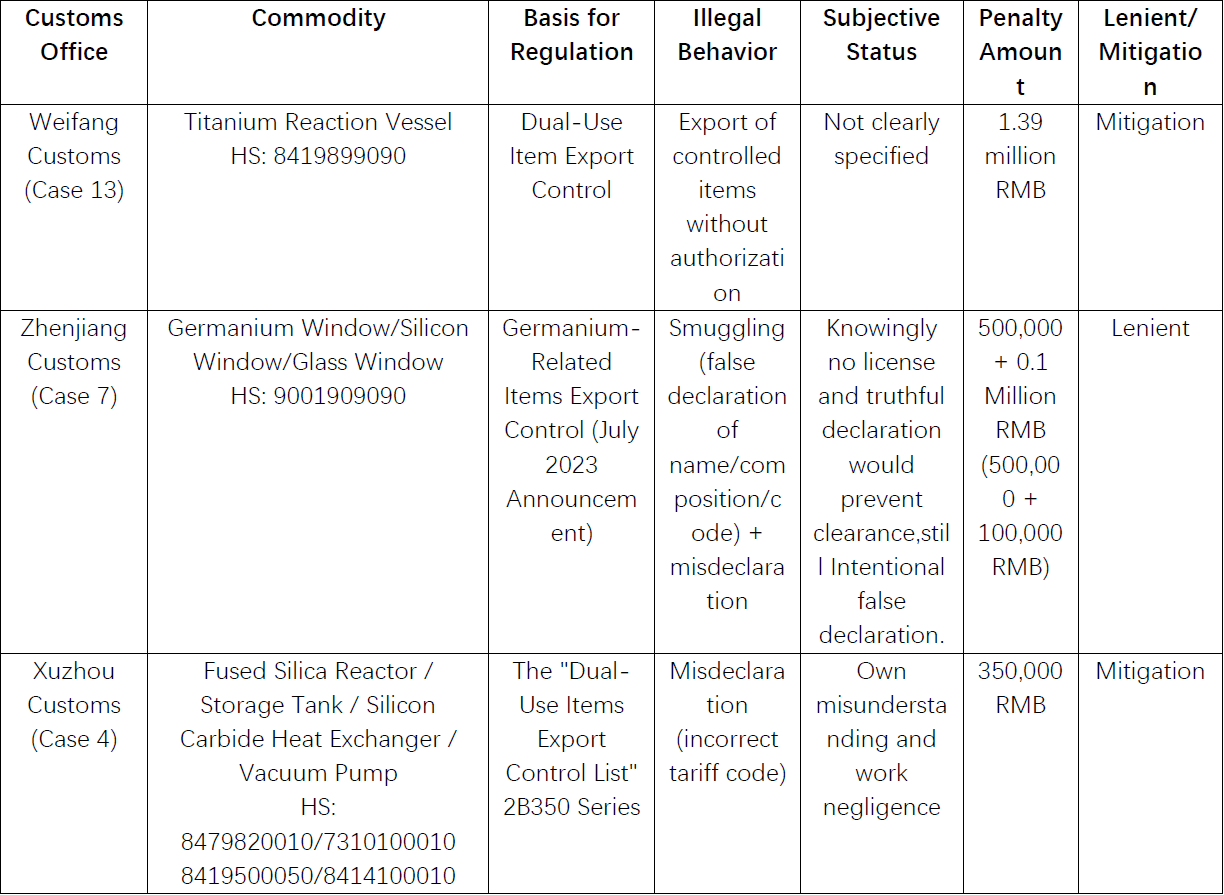

(I) Filing Differences in Three Export Control Cases

Table 5: Export Control Case Comparison Table

(II)Why was the Company Z deemed as smuggling, whereas the other two cases were considered violations of regulations

In the case of company Z (Case 7), the party was aware that exporting elemental germanium required a Dual-Use Item License. Despite knowing that "no license could be obtained and truthful declaration would prevent clearance," the party still proceeded to declare by "vaguely stating the product name, falsely declaring the composition and commodity code."

In the case of company E (Case 13), the party made misdeclarations of tariff code due to "its own misunderstanding and work negligence." It declared controlled items that should have been classified under 8479820010, 7310100010, 8419500050, and 8414100010 as 8419899090 or 8414100090. Although the party did not apply for a license, there is no evidence indicating a subjective intent to falsely declare the product name/composition in order to evade regulation. The tariff code errors might be caused by various technical issues and have not been classified as "false declaration".

Case W (Violation) (Case 4): The party declared a titanium reaction kettle as 8419899090, while actually involved the export control of dual-use items.

The parties did not have any situation of misdeclaration of product name, ingredients and tariff code. However, they were identified as "unauthorized export of controlled items without authorized". In this case, although the customs still used the term "misdeclaration" in the name, there were no specific items that were false declared. The customs ultimately applied the default mitigating clause in the Administrative Penalty Law to the parties.

In conclusion, in the case of Company Z (Case 7), the product name, composition, and commodity code were all falsely declared. This is more persuasive in establishing the subjective intent to evade export control regulations compared to the case of Company E (Case 13), where only the tariff code was misdeclared, and the case of No declaration of Company W (Case 4). The reason is that when all the underlying objective facts deviate, it necessarily undermines the enforcement of export control regulations based on the factual composition and technical parameters. Therefore, the intent to smuggle is clearly evident, as such deviations from all objective facts are not acceptable for production/export enterprises that have numerous legal obligations.

(III) Is There a Renewed Trend Toward Leniency in Export Control Penalties?

As can be seen from the above, not only in the Company E case (Case 13) and the Company W case (Case 4), where the customs only imposed fines under the first item of Article 34(1) of Export Control Law was applied (a fine of 5 to 10 times the amount of illegal business operations)[7] , but also in the Company Z case (Smuggling) (Case 7), where the fine of 500,000 RMB was imposed. It was also the lower limit of the general administrative penalty applicable in cases of unauthorized export of dual-use items..

Compliance Signal 6: The Difficulty in Determining Intent in Cases Involving Solid Waste

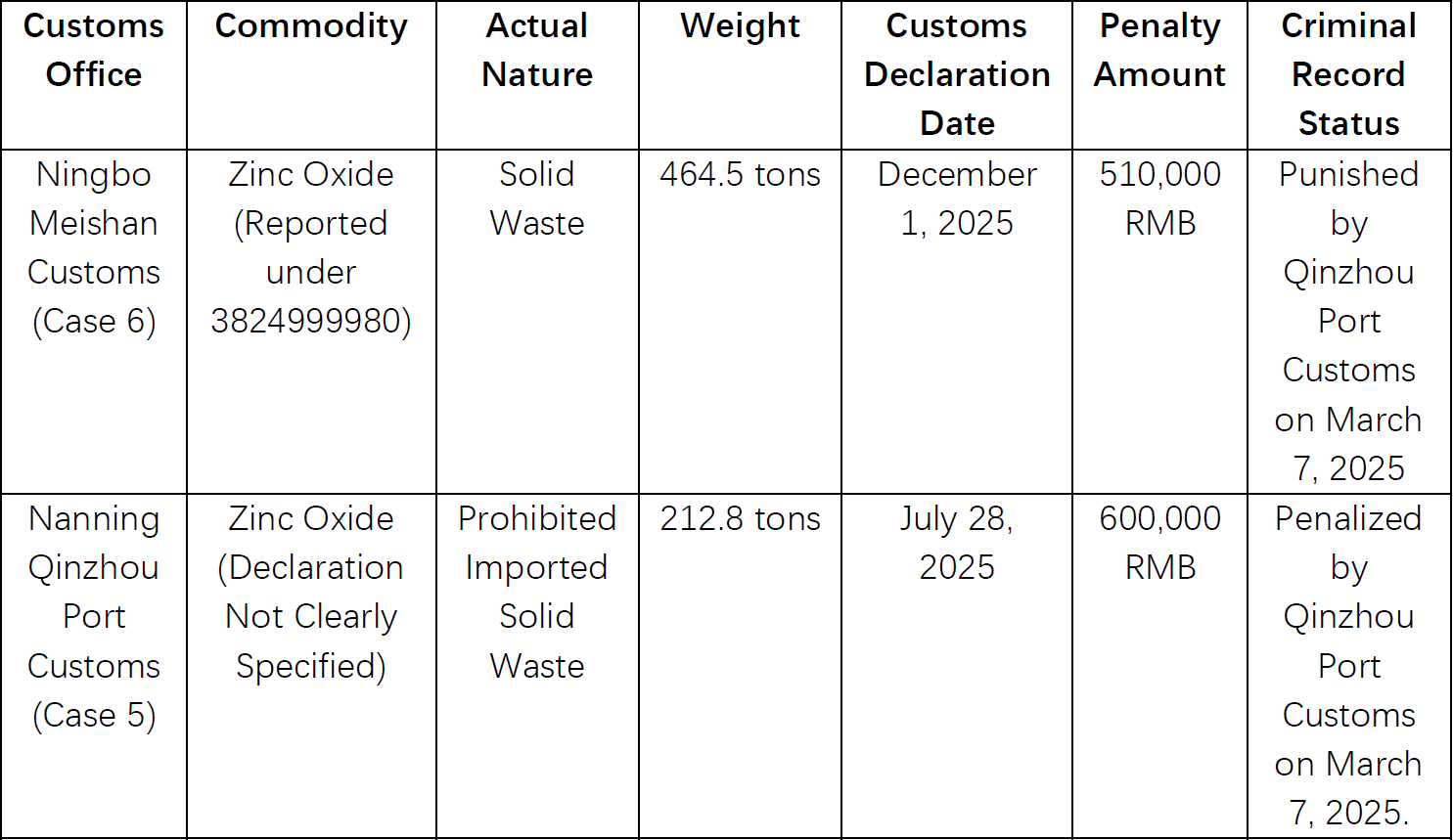

(I) Repeated Illegal Acts at Two Ports by the Same Enterprise

Table 6: Comparison of Company S's Solid Waste Cases

(II) Why Was It Not Classified as Smuggling?

Company S was penalized three times for importing the same (similar) solid waste at Meishan Customs (December 2025) and Qinzhou Port Customs (March & July 2025). Why was it not deemed smuggling? The possible reason may be the sources of goods are different. the goods were identified as solid waste only after inspection by customs, and it may have been unknown at the time of importation; there is no other evidence to prove that the party was "aware" that it was solid waste and intentionally imported it.

Moreover, the final administrative penalty was lenient. In the Meishan Customs case (Case 6) (510,000 RMB), the penalty was mitigated under Article 17(1) of The Discretion Benchmark of Customs for Administrative Penalties (I) (mitigation)[8]. In the Qinzhou Port Customs case (Case 5) (600,000 RMB), there were two aggravating circumstances (recidivism within one year, quantity over 200 tons) and one mitigating circumstance (re-export within two months), and the final penalty was applied as "leniency."

(III) Article 13 of The Implementation of Customs Administrative Penalty No Longer Applies to The Import of Solid Waste.

Article 115 of Law on the Prevention and Control of Environmental Pollution by Solid Wastes that "importing foreign solid waste into the territory shall be punished by a fine of between RMB 500,000 yuan and RMB 5,000,000 yuan"; Article 13 of the Implementation of Customs Administrative Penalty provides that "where a party imports or exports goods prohibited from import or export by the state in violation of national import and export management regulations, the goods shall be ordered to be returned and a fine of up to RMB 1,000,000 yuan shall be imposed." The two laws clearly conflict: according to the "new law prevails over old law" and "special law prevails over general law" principles under the Legislation Law, the 2020 revised Law on the Prevention and Control of Environmental Pollution by Solid Wastes, as a newer and more specific law, shall be applied with priority, demonstrating a higher penalty ceiling to reflect strict regulation of the import of solid waste.

Based on the above comparison, the author believes that this case demonstrates that the strict attitude shown by the law and the evidence standards actually applied by the customs in handling cases must not deviate from each other, and they must not be confused.

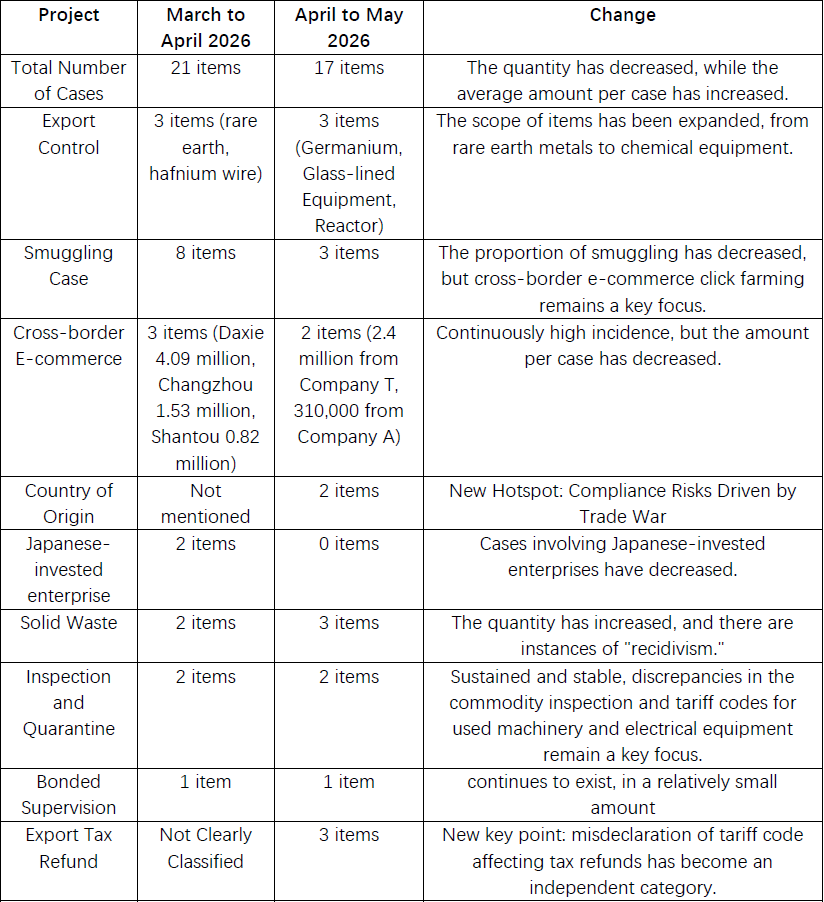

VII. Summary: Changes and Trends of This Case Compared to the Previous Period

(I) Comparison with the Case of March-April 2026

Table 7: Comparative of the Two Cases

(II) New Issues Brought by Discretion Refinement

In addition to the characteristics reflected in the classification analysis, it should be noted that these high-value cases exhibits the feature of "more refined application of discretionary benchmarks." Complex discretionary scenarios have emerged, such as "segmented handling" (in the case of Company M (Case 2), matters were handled separately according to time periods) and "comprehensive consideration of multiple factors" (Company S (Case 5), where aggravating and mitigating factors resulted in a mitigated penalty). However, the refinement also brings new issues: the coexistence of mitigation and general discretionary standards (in the case of Company L (Case 15), mitigation was applied; in the case of Company Y (Case 17), general circumstances were considered), the final penalty being inconsistent with the standard applied after the assessment (in the Meishan Customs case of Company S (Case 6), 5.1 million was mitigated), and so on.

VIII. Corporate Compliance Recommendations

(I) Establishment of an Origin Traceability System: For sensitive goods such as integrated circuits, semiconductors, and electronics, establish complete supply chain documentation from wafer manufacturing to packaging and testing, to ensure that origin declarations can be verified.

(II) Strengthening Export Control Screening: For chemical equipment, metal products, electronic components, and other items, establish a screening mechanism for dual-use items, and confirm whether a license is required prior to export. Special attention is drawn to the fact that in July 2023, the Ministry of Commerce implemented export controls on gallium, germanium-related items, and in 2024, expanded controls to graphite, rare earths, etc. Enterprises must promptly update their controlled item lists.

(III) Eliminate Cross-Border E-Commerce Click farming: Strictly distinguish the boundaries between general trade and cross-border e-commerce retail imports, and prohibit the use of individual identity quotas to split orders.

(IV) Zero Tolerance for Import of Solid Waste: Establish mechanisms for supplier review and cargo pre-inspection to ensure that imported goods are not solid waste, thereby avoiding enhanced penalties for repeat offenders.

(V) Seizing the Leniency Window of "Cooperation + Admission of Guilt and Penalty Acceptance": the four requirements—first-time violation, voluntary reporting, cooperation with investigation, and payment of arrears—must all be fulfilled to expect leniency; resistance to law enforcement, destruction of evidence, or reoffending within one year will result in aggravated punishment.

(VI) Pay Attention to the Risk of Administrative-Criminal Linkage: In smuggling cases, even after administrative penalties have been completed, it is still necessary to pay attention to whether the case is still within the criminal prosecution period. One should not misjudge that "the completion of administrative proceedings means safety."

(VII) Standardization of Document Citation Provisions: It is recommended that the customs authorities in the penalty decision document: clearly distinguish between "penalty level" and "calculation method"; provide additional reasoning for "the more severe penalty applies"; correct erroneous expressions such as "revised discretion benchmark"; and explain instances where "there is no illegal gains" or "illegal gains are difficult to calculate."

This report is compiled based on 17 publicly issued administrative penalty decisions by customs offices nationwide from April to May 2026. It focuses on examining the logical consistency of the application of relevant provisions and the accuracy of the discretion benchmarks. Due to limited disclosure in some case documents, not all details have been fully covered. Therefore, this analytical opinions is provided herein for the reference of company compliance and does not constitute legal advice.

[Note]

[1] Company G (Case 9) and Company H (Case 10) are both state-owned enterprises. Their nature of the enterprises can be confirmed by the unified social credit code and names listed in the penalty decision document.

[2] Article 15 of Regulation of the People's Republic of China on the Implementation of Customs Administrative Punishment: Whoever fails to declare the commodity name, tariff number, quantity, specification, price, mode of trade, place of origin, place of departure, place of arrival, final destination, or other items of imported or exported goods which should have been declared to the Customs or falsely declares such information shall be punished in accordance with the following provisions respectively and the illegal income, if any, shall be confiscated: (5) Whoever affects the state's administration of foreign exchange and export tax refund shall be fined not less than 10% nor more than 50% of the declaration price.

[3] Article 36 of Administrative Sanctioning Law of the People's Republic of China: Where any illegal conduct is not discovered within two years, administrative sanctions are no longer imposed.

[4] Article 33 of Administrative Sanctioning Law of the People's Republic of China: Where a party has sufficient evidence to prove that the party has no subjective fault, the party is exempted from administrative sanctioning, except as otherwise provided for by a law or administrative regulation.

Article 7 of Announcement No. 182 [2023] of the General Administration of Customs―Announcement on Issuing the Discretion Benchmark of the Customs of the People's Republic of China for Administrative Penalties (I): A party falling under any of the following circumstances shall be exempted from an administrative penalty: 3. The party has sufficient evidence to prove that he or she has no subjective fault. If it is otherwise prescribed by any law or administrative regulation, such provisions shall prevail.

[5] Article 15 of Regulation of the People's Republic of China on the Implementation of Customs Administrative Punishment: Whoever fails to declare the commodity name, tariff number, quantity, specification, price, mode of trade, place of origin, place of departure, place of arrival, final destination, or other items of imported or exported goods which should have been declared to the Customs or falsely declares such information shall be punished in accordance with the following provisions respectively and the illegal income, if any, shall be confiscated: (3) Whoever affects the state's licensing administration shall be fined not less than 5% nor more than 30% of the value of the goods. (5) Whoever affects the state's administration of foreign exchange and export tax refund shall be fined not less than 10% nor more than 50% of the declaration price.

[6]Article 18 of Regulation of the People's Republic of China on the Implementation of Customs Administrative Punishment: Whoever commits any of the following acts shall be fined not less than 5% nor more than 30% of the value of the goods and the illegal income, if any, shall be confiscated:

(1) Opening, picking up, delivering, shipping, exchanging, repacking, mortgaging, pledging, holding as a lien, transferring, altering marks, using for other purposes, or otherwise disposing of goods subject to customs supervision without the permission of the Customs.

[7] Article 34 of Export Control Law of the People's Republic of China: An export business which commits any of the following conduct shall be ordered to cease the violation of law, and with any illegal income therefrom confiscated, fined not less than five nor more than ten times its illegal turnover if the illegal turnover is 500,000 yuan or more or fined not less than 500,000 yuan nor more than five million yuan if there is no such illegal turnover or the illegal turnover is less than 500,000 yuan; and if the circumstances are serious, shall be ordered to cease its business operation for an overhaul, and even disqualified for the export of the relevant controlled items: (1) Exporting any controlled item without being licensed.

[8]Article 17 of Announcement No. 182 [2023] of the General Administration of Customs―Announcement on Issuing the Discretion Benchmark of the Customs of the People's Republic of China for Administrative Penalties (I): In a case involving the illegal import of solid wastes into China, as handled in accordance with Articles 115 and 116 of the Law on the Prevention and Control of Solid Wastes, the penalty shall be determined in accordance with the following provisions: 1. If a mitigated administrative penalty is imposed, a fine of less than 500,000 yuan shall be imposed.