ARTICLES

Steering the Ship: China Retroactively Blocks the Foreign Acquisition of an AI Agent Project

Steering the Ship: China Retroactively Blocks the Foreign Acquisition of an AI Agent Project

Recently, the Office of the Foreign Investment Security Review Working Mechanism under China’s National Development and Reform Commission (“NDRC”) issued a decision to prohibit the foreign acquisition of an AI agent project (“Project M”) and ordered the parties to revoke and unwind the transaction. The foreign investor in Project M had previously announced the completion of the acquisition in late 2025. This prompted China’s Ministry of Commerce to declare in early 2026 that it would work with relevant authorities to conduct compliance assessments and investigations against the acquisition.

I.Transaction Overview

In this transaction, the foreign acquirer is a major U.S. technology platform company that owns several of the world’s mainstream social media and instant messaging applications, but lacks an AI agent product capable of integrating these platforms and performing tasks across them. Project M is a general-purpose AI agent product that can autonomously plan, break down and execute complex tasks in a virtual environment. The foreign acquirer stated that the cooperation would “unlock opportunities for businesses across our products.”

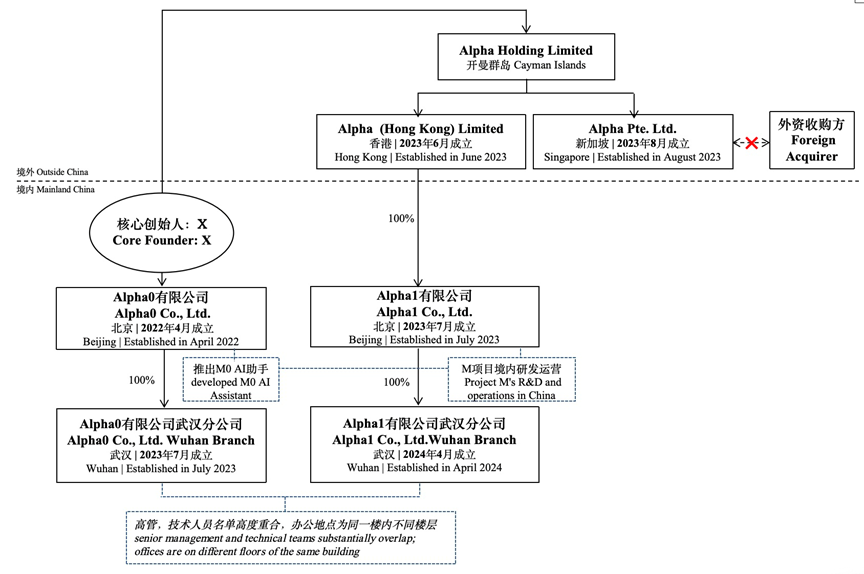

According to publicly available information and media reports, Project M originated in China and has maintained deep ties with Chinese entities, R&D teams and product technology accumulation. The evolution of Project M may be illustrated in the chart below.

Chart 1: Illustrative Transaction Structure of Project M (Based on Relevant Corporate Registration Records and Media Reports)

In April 2022, the core founder X, a graduate of a university in Wuhan, established Beijing Alpha0 Co., Ltd. and launched M0, an AI assistant product. This helped the team gain experience in AI agent product development and operations in China. In 2023, the founding team set up a foreign shareholding structure and established Alpha1 Co., Ltd. in Beijing, China, through a Hong Kong entity, Alpha (Hong Kong) Limited, as the domestic R&D and operating entity for Project M. According to Project M’s official website, only 8 months after its official launch, Project M had exceeded US$100 million in annual recurring revenue (ARR). Probably driven by considerations to facilitate overseas operations and cross-border financing, in the same year of 2023, the founding team further established a Singapore company, Alpha Pte. Ltd., as the overseas operating entity for Project M. Alpha later moved its headquarters to Singapore and obtained US$75 million in financing. Meanwhile, the China-based team was gradually dissolved, while the China-based entities have been retained and remain in existence to date. By then, after its incubation, Project M and Alpha had completed a “de-Chinafication” restructuring. In the end, Project M was acquired by foreign capital in Singapore for approximately US$2 billion. This Singapore-based “de-Chinafication” model has been called “Singapore washing.”

II. The Foreign Investment Security Review Regime Came into Play

China’s foreign investment security review mechanism is a legal system designed to review foreign investments that affect or could affect national security. The Office of the Foreign Investment Security Review Working Mechanism (“Working Mechanism Office”) is responsible for the day-to-day review. Under Article 2 of the Measures for the Security Review of Foreign Investment (“Review Measures”), this mechanism is triggered if the following criteria are met: (i) the investor is a foreign investor; (ii) the foreign investor directly or indirectly invests in China, including acquiring equity interests or assets of a domestic enterprise through M&A and investing in China by other means; and (iii) such investment affects or could affect national security.

Project M’s R&D team, algorithms, data and operational experience all constituted core assets of Alpha. Although these assets were transferred outside China through restructuring, this restructuring did not go through relevant approval procedures such as outbound investment registration, technology export licensing, and data export security assessment. Therefore, these assets remain as assets of a Chinese enterprise. The foreign acquisition of Project M will result in the assets of a domestic enterprise being controlled by a foreign investor through acquisition, which constitutes an indirect investment within China by a foreign investor. This foreign investment will trigger China’s foreign investment security review, if it affects or could affect national security.

To clarify, while setting up the foreign shareholding structure for Project M resulted in the assets of a Chinese entity being controlled by a Singaporean company, this restructuring did not trigger China’s foreign investment security review, because at that time the actual controller of Project M remained a Chinese controller (unless the actual controller changed nationality).

III. Why the Transaction Raised National Security Concerns

Why would this transaction rise to the level of national security? The answer should be given from the broader perspective of the so-called U.S.-China AI race. The U.S.-China AI race is a full-spectrum competition spanning from computing power, large language models, data to ecosystems. The United States focuses more on artificial general intelligence and has advantages in general-purpose foundation models and platform entry points. China, by contrast, places greater emphasis on integrating AI with industrial systems, application scenarios and data resources, and is competitive in scenario application. Overall, both the U.S. and China have their comparative strengths in the AI race, and the gap between them becomes narrower. Thus, the U.S.-China AI race remains highly contested.

Against this background, if the Project M transaction were allowed to stand, it would mean that an AI startup that completed its early-stage incubation in China could be acquired by a U.S. platform company through a “de-Chinafication” arrangement, thereby helping a competitor fill its gaps in AI scenario applications and AI agent products, and ultimately strengthening that competitor’s ecosystem at China’s own cost. Project M would not only allow some of the most valuable application innovation capabilities in China’s AI ecosystem to be systematically absorbed into the U.S. AI ecosystem, but its “Singapore washing” model could also have potential impact and demonstrative effect on the U.S.-China AI race. If such model were replicated, China might lose strength in taking the path of focusing on applications in the AI race, and could ultimately fall behind. Therefore, Chinese AI companies going global are not merely a matter of a single company or a single transaction, but may become a delicate issue affecting the overall U.S.-China AI race.

Likewise, if a major Chinese technology company were to indirectly acquire a U.S. AI startup, the United States would likely adopt the same regulatory stance. Through mechanisms such as the Committee on Foreign Investment in the United States (CFIUS), it would review the transaction from the perspectives of critical technologies, sensitive data, supply chain security and national security, and further block the transaction.

IV. Conclusions and Takeaways

As the U.S.-China AI race extends from technology to industrial ecosystems, foreign investment security review is becoming an important variable that AI companies cannot afford to ignore when pursuing cross-border financing and international technology cooperation. Against this background, Chinese AI companies should formulate their going-global strategies from the perspectives of the overall U.S.-China AI race and China’s national industrial security. “De-Chinafication” through arrangements such as “Singapore washing” does not place a transaction outside the reach of Chinese regulatory oversight.

Further, China does not restrict companies from carrying out overseas market development, foreign financing, or international technological cooperation (including technology licensing transactions). However, for Chinese AI companies, relevant foreign financing arrangements and international technological cooperation should be premised on not losing control over their ownership or key technologies. In particular, companies with critical value in the AI industrial ecosystem must always steer the ship themselves.